How do checking and savings accounts work, and how can you do basic accounting?

Many individuals use bank accounts without really knowing how they work or why they are important, yet money is a huge element of almost everything we do every day. Things like bank accounts, savings accounts, accounting records, and even the phrase "charged off" can be scary at first. But they aren't too hard to figure out if you look closely. Bank accounts can be compared to various tools in a toolbox. Using the proper tool at the right time makes it much easier and less stressful to handle your money.

These days, having at least one bank account isn't a luxury; it's a must. You can pay your bills online, get your paychecks by email, and even buy a cup of coffee with your phone or card. Understanding the pros and drawbacks of checking accounts, the purpose of savings accounts (especially from a financial literacy perspective like EverFi), and the main differences between the two will help you make better financial decisions. Also, knowing how to do basic accounting and what it means to have a charged-off account will help you avoid making mistakes that will hurt your credit and cost you money for a long time. and here is how to open a bank account and handle your money on a daily basis

This essay uses real-life examples and clear explanations to break down everything you need to know. This essay doesn't rely heavily on technical terms. You don't have to have a degree in finance. Just useful information that everyone can understand.

The Benefits of Having a Checking Account

Your checking account is the most important part of your daily money. You can use this account to receive payments, settle bills, purchase groceries, or send money to a friend. The best thing about a checking account is how simple it is to use. It should let your money move quickly, smoothly, and safely.

You can still get to your money right away, but a checking account is a safer place to keep it than your home or wallet. You can pay bills online, write a check, get cash from an ATM, or use a debit card in just a few seconds. That level of freedom is hard to beat. It seems like you have a place to keep track of your money without having to do anything.

Being in command is another big benefit. With online and mobile banking, you can see right away how much money you've spent. You can see exactly where your money goes, which makes it easier to stick to your budget and not spend too much. Many banks will also send you alerts when your balance is low, you buy something big, or something strange happens. Such functionality makes things even safer and more aware.

Checking accounts are just as important for everyday life. Many employers encourage you to use direct deposit. Landlords and utility companies want you to pay them online. Every month, subscription services automatically take money out of your bank account. It might be hard and annoying to keep track of these everyday money problems without a checking account. A checking account is a great way to manage your money and stay current with the economy.

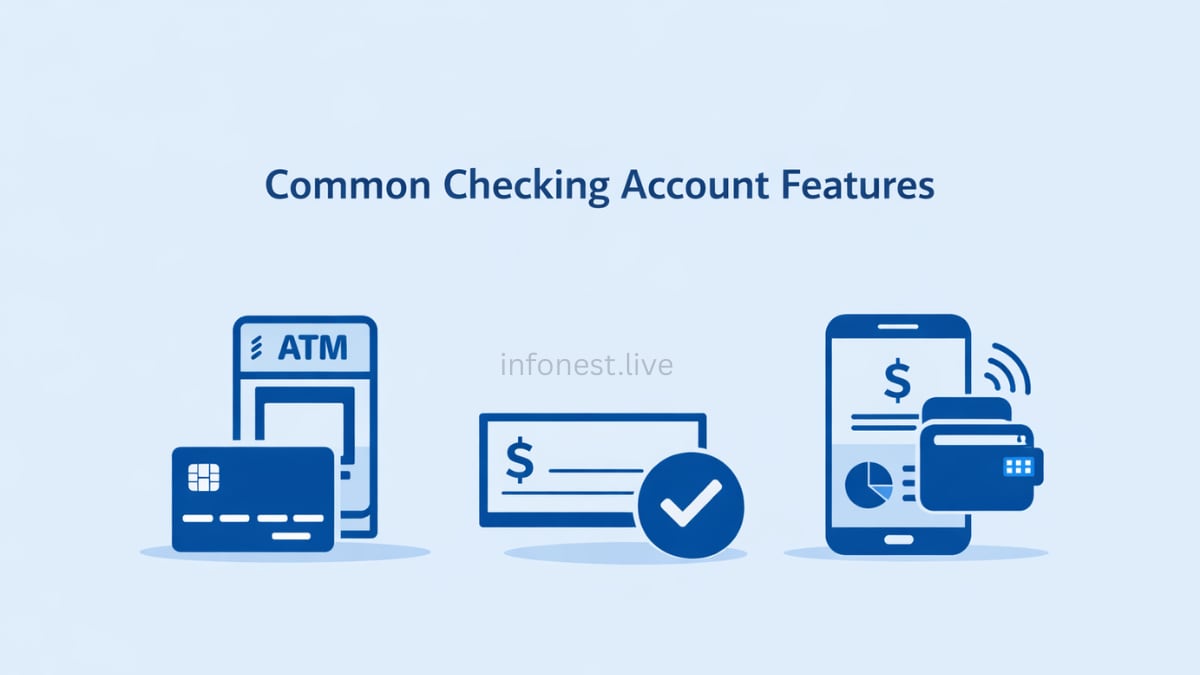

Most checking accounts have the following features:

Every day, you can choose from several different options with a checking account. The debit card is one of the most popular. This card lets you get cash right away, whether you're at a store, an ATM, or buying something online. You are using money you already have, which means you won't get into debt as you would with a credit card.

Checks are another classic thing. Checks are less common now, but they can still be useful for paying rent, giving gifts, or paying when online payment isn't an option. Paying bills online is another helpful tool. You may pay all of your bills from your checking account in one place instead of having to write checks or log into different websites.

People use their checking accounts in a completely different way now that they have apps for their phones. You can deposit a check, send money immediately, and monitor your transactions while on the move. Digital wallets are also accepted by many banks, enabling you to make payments without the need to remove your phone or watch.

All of these things work together to make checking accounts quite helpful. People consider them to be their main account because they are quick, easy to get to, and used a lot.

How to Keep an Eye on Your Checking and Savings Accounts

Only accountants may care about accounting entries, which are just a way to track money's source and destination. To keep track of your money and stay organized, you need to know how to do basic accounting. This principle is true no matter whose money you are in control of.

Debits and credits are the most important parts of accounting. Putting money into your bank or savings account is an increase. You lose money when you spend it. It might be as straightforward as writing down a rent payment or a bank transfer for your money. It makes things easier for businesses, but it still makes sense.

For example, if you put $1,000 in your checking account and then took out $1,000 from it,

Credit: A cash or income amount of $1,000

When you pay your $150 utility bill, $150 goes toward the cost of utilities.

Credit: $150 to the checking account

There are many reasons to have a savings account, but they all work the same way. Putting money into savings is usually considered a transfer, not an expense. This difference helps you understand that saving is not the same as spending; it is putting money aside for later.

If you know these important entries, you'll be able to see things more clearly. You can now see where your money went, so you don't have to worry. When you turn on a light in a dark room, everything becomes clear.

What does it mean when an account is charged off?

"Charged off" seems like a huge deal, and it kind of is. When a lender writes off an account, it means they don't think they can get the money back. This procedure usually happens after a lot of payments are missed, which is usually after 180 days.

The most important thing to understand is that the debt doesn't go away just because an account is charged off. You still have to pay. The lender just pulls the money out of their active accounts and calls it a loss for tax purposes. From your perspective, these things can really affect your credit and money.

Your credit score goes down a lot when you charge off. It tells lenders that you didn't pay back a loan like you said you would. The loan that has been charged off could potentially go to collectors, which would hurt your credit score even more. These events can make it harder to find a job, rent an apartment, or even secure a loan.

Knowing about charge-offs makes you realize how important it is to keep your savings and checking accounts in good health. Overdrafts, late payments, and poor cash flow management can all cause money problems that last a long time. If you closely monitor and manage your accounts, you may be able to prevent issues that initially lead to charge-offs.

EverFi thinks that having a savings account has many benefits.

EverFi's lectures on how to handle money indicate that a savings account is largely about being safe and getting ready. You can use a checking account now and a savings account later. The nicest thing about it is that it helps you save money.

The best place to keep money for emergencies is in a savings account. Life happens: cars break down, health problems come up, and jobs change. If you have money saved up in a savings account, these surprises won't turn into money issues. EverFi talks about saving cash a lot because it makes people stronger and less reliant on loans and credit cards.

You can also gain money by earning interest. The interest on your savings account won't make you rich right away, but it will help your money grow on its own. Just sitting there makes your balance slowly go up, which is a great method to learn how to save. It's like planting a tree. It takes time to grow, but it's worth it.

Savings accounts could also help you stick to your plans. You shouldn't use them every day, so they make you think before you take out money. That break is really strong. It teaches you to put long-term ambitions ahead of short-term needs. This is an important lesson in how to handle your money.

What Sets a Checking Account Apart from a Savings Account

There is a difference between a savings account and a checking account. You can use money from a checking account to buy things. A savings account lets you save money. One is full of energy and moves quickly, while the other is calm and steady.

People who do a lot of business have checking accounts. You can normally put money in and take it out whenever you want. Most of the time, you can only take money out of a savings account a certain number of times each month. This isn't a problem; it's a good thing. It keeps your money safe and stops you from buying things you don't need.

Another big difference is interest. Most of the time, checking accounts don't earn any interest. If you don't touch your money, savings accounts provide you higher interest. The costs can also be different. For instance, checking accounts can charge you for going over your limit, while savings accounts might focus on how much money you can store in them.

If you know the difference, you will be able to use each account correctly. You could spend too much money or miss out on growth if you mix up their goals. If you use them right, they work well together.

To put it briefly, being successful with money requires knowing how to use checking and savings accounts.

Checking and savings accounts can do more than just keep your money safe. They are very important for making money and keeping it in excellent shape. A checking account helps you get through the day, while a savings account lets you plan for the future and the things that come up. If you know what a charge-off is and how to look at accounting documents, you might be able to prevent big money problems.

Using these accounts lets you control your money instead of wondering where it went. Being in charge makes you feel better about yourself, lowers your stress, and gives you new ways to make money. Once you understand the basics, everything else is simple.

Many people want to know these things.

- Can I have more than one checking and savings account?

Yes, many people have more than one account to help them keep track of their expenses, spending, and savings goals. - Is it safer to put your money in a savings account than in a checking account?

If you have insurance on either of them, they are usually safe enough. But savings accounts make it less likely that you'll spend money. - Do charge-offs ever go away?

They stay on your credit report for years, even after you pay them off. However, their impact gradually decreases over time. - Should I keep all of my money in my checking account?

No, separating savings helps keep money safe and encourages excellent habits. - Are internet savings accounts better than regular ones?

You should also consider how easy it is to get there and what you like, even if they usually have higher interest rates.